17.7 Multicollinearity

Multiple regression assumes that the independent variables are not highly correlated with each other.

17.7.1 The problem

Collinearity: High correlation exists among two or more independent variables.

This means the correlated variables contribute redundant information to the multiple regression model.

Including two highly correlated explanatory variables can adversely affect the regression results:

- No new information provided

- Can lead to unstable coefficients (large standard error and low t-values)

- Coefficient signs may not match prior expectations

Multiple linear regression assumes that there is no multicollinearity in the data.

Multicollinearity occurs when the independent variables are too highly correlated with each other.

After reading this Section you will be able to:

- Identify collinearity in multiple linear regression.

- Understand the effect of collinearity on regression models.

17.7.2 Exact collinearity

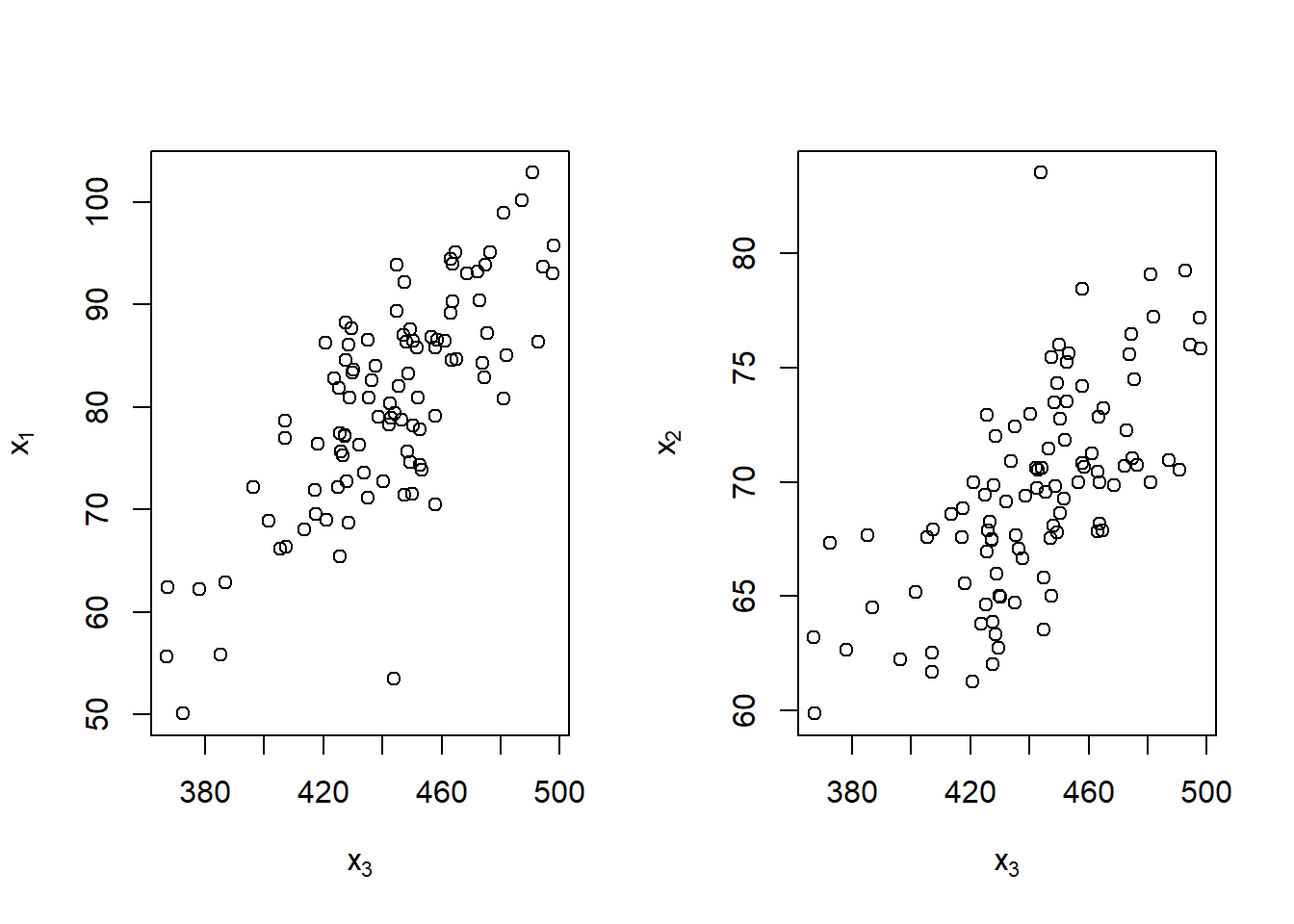

Let’s create a dataset where one of the predictors, \(x_3\), is a linear combination of the other predictors, \(x_1\) and \(x_2\):

\[x_3 = 2 \times x_1 + 4 \times x_2 + 3\]

| \(y\) | \(x_1\) | \(x_2\) | \(x_3\) |

|---|---|---|---|

| 170.7135 | 93.70958 | 76.00483 | 494.4385 |

| 152.9106 | 74.35302 | 75.22376 | 452.6011 |

| 152.7866 | 83.63128 | 64.98396 | 430.1984 |

| 170.6306 | 86.32863 | 79.24241 | 492.6269 |

| 152.3320 | 84.04268 | 66.66613 | 437.7499 |

| 151.3155 | 78.93875 | 70.52757 | 442.9878 |

What happens when we attempt to fit a regression model using all of the predictors?

\[y_i = \beta_0 +\beta_1x_{1i}+\beta_2x_{2i}+\beta_3x_{3i}+\epsilon_i\]

.

. Call:

. lm(formula = y ~ x1 + x2 + x3, data = exact_collin_data)

.

. Residuals:

. Min 1Q Median 3Q Max

. -2.57662 -0.66188 -0.08253 0.63706 2.52057

.

. Coefficients: (1 not defined because of singularities)

. Estimate Std. Error t value Pr(>|t|)

. (Intercept) 2.957336 1.735165 1.704 0.0915 .

. x1 0.985629 0.009788 100.702 <2e-16 ***

. x2 1.017059 0.022545 45.112 <2e-16 ***

. x3 NA NA NA NA

. ---

. Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

.

. Residual standard error: 1.014 on 97 degrees of freedom

. Multiple R-squared: 0.9923, Adjusted R-squared: 0.9921

. F-statistic: 6236 on 2 and 97 DF, p-value: < 2.2e-16When this happens, we say there is exact collinearity in the dataset.

As a result of this issue, the software used here \(R\) essentially chose to fit the model without \(x_3\).

. Warning: Model matrix is rank deficient. Parameters x3 were not estimable.| y | ||||

|---|---|---|---|---|

| Regressor | \(\hat \beta\) | std. Error | \(t_{stat}\) | \(p\)-value |

| (Intercept) | 2.96 | 1.74 | 1.70 | 0.0915 |

| x1 | 0.99 | 0.01 | 100.70 | <0.001 |

| x2 | 1.02 | 0.02 | 45.11 | <0.001 |

| Observations | 100 | |||

| R2 / R2 adjusted | 0.992 / 0.992 | |||

However notice what two other models would accomplish exactly the same fit:

- Model 1: \(y_i = \beta_0 +\beta_1x_{1i}+\beta_2x_{2i}+\epsilon_{i1}\)

- Model 2: \(y_i = \beta_0 +\beta_1x_{1i}+\beta_3x_{3i}+\epsilon_{i2}\)

- Model 3: \(y_i = \beta_0 +\beta_2x_{2i}+\beta_3x_{3i}+\epsilon_{i3}\)

| y | y | y | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable | Estimates | std. Error | p-value | Estimates | std. Error | p-value | Estimates | std. Error | p-value |

| (Intercept) | 2.96 | 1.74 | 0.092 | 2.19 | 1.75 | 0.213 | 1.48 | 1.74 | 0.398 |

| x1 | 0.99 | 0.01 | <0.001 | 0.48 | 0.02 | <0.001 | |||

| x2 | 1.02 | 0.02 | <0.001 | -0.95 | 0.03 | <0.001 | |||

| x3 | 0.25 | 0.01 | <0.001 | 0.49 | 0.00 | <0.001 | |||

| Observations | 100 | 100 | 100 | ||||||

| R2 / R2 adjusted | 0.992 / 0.992 | 0.992 / 0.992 | 0.992 / 0.992 | ||||||

We can observe that the fitted values for each of the three models are exactly the same. This is a result of \(x_3\) containing all of the information from \(x_1\) and \(x_2\). As long as one of \(x_1\) or \(x_2\) are included in the model, \(x_3\) can be used to recover the information from the variable not included.

| Model 1 | Model 2 | Model 3 |

|---|---|---|

| 172.6216 | 172.6216 | 172.6216 |

| 152.7488 | 152.7488 | 152.7488 |

| 151.4793 | 151.4793 | 151.4793 |

| 168.6395 | 168.6395 | 168.6395 |

| 153.5956 | 153.5956 | 153.5956 |

| 152.4923 | 152.4923 | 152.4923 |

While their fitted values are all the same, their estimated coefficients are wildly different. The sign of \(x_2\) is switched in two of the models! So only Model 1 properly explains the relationship between the variables, Model 2 and Model 3 still predict as well as Model 1 despite the coefficients having little to no meaning15, since the real model used to generate the dataset is:

\[ y_i = 3 + x_{1i}+ x_{2i}+ \epsilon_i, \epsilon_i \sim N(0,1)\]

Exact collinearity is an extreme example of collinearity, which occurs in multiple regression when predictor variables are highly correlated. Collinearity is often called multicollinearity, since it is a phenomenon that really only occurs during multiple regression.

17.7.3 Indicators of Multicollinearity

- Coefficients differ from the values expected by theory or experience, or have incorrect signs.

- Coefficients of variables believed to be a strong influence have small \(t\) statistics indicating that their values do not differ from 0.

- All the coefficient student \(t\) statistics are small, indicating no individual effect, but the overall \(F\) statistic indicates a strong effect for the total regression model.

- High correlations exist between individual independent variables or one or more of the independent variables have a strong linear regression relationship to the other independent variables or a combination of both.

17.7.4 Detecting Multicollinearity

- Examine the simple correlation matrix to determine if strong correlation exists between any of the model independent variables.

- Look for a large change in the value of a previous coefficient when a new variable is added to the model.

- Does a previously significant variable become insignificant when a new independent variable is added?

- Does the estimate of the standard deviation of the model increase when a variable is added to the model?

17.7.5 Corrections for Multicollinearity

- Remove one or more of the highly correlated independent variables.

- Change the model specification, including possibly a new independent variable that is a function of several correlated independent variables.

- Obtain additional data that do not have the same strong correlations between the independent variables.

17.7.6 Our Monet Case

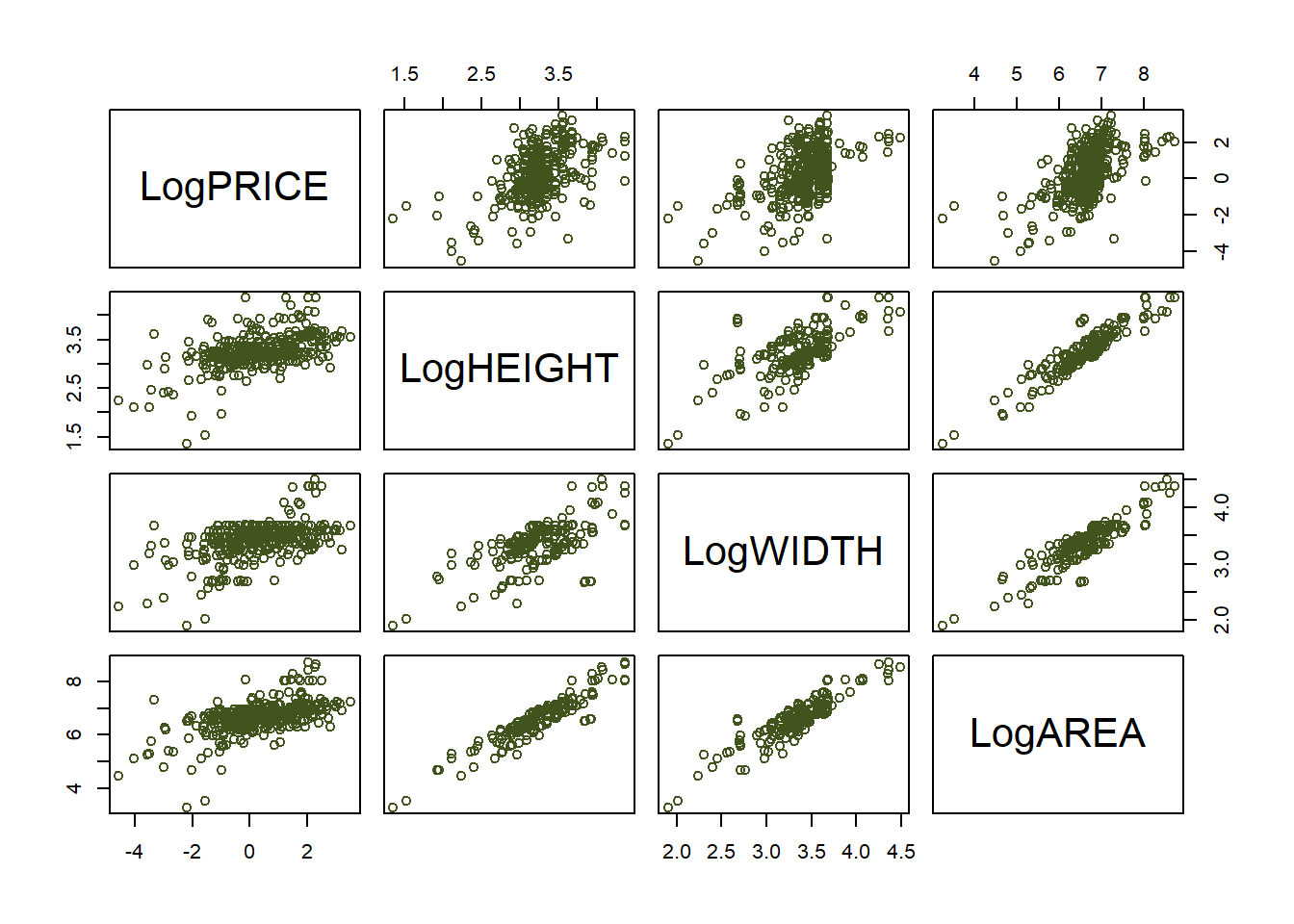

Using the Case described in @ref{monet}, we use Multiple Linear Regression to model the relationship between PRICE and the rest of variables in the dataset.

| PRICE | HEIGHT | WIDTH | SIGNED | PICTURE | HOUSE |

|---|---|---|---|---|---|

| 3.993780 | 21.3 | 25.6 | 1 | 1 | 1 |

| 8.800000 | 31.9 | 25.6 | 1 | 2 | 2 |

| 0.131694 | 6.9 | 15.9 | 0 | 3 | 3 |

| 2.037500 | 25.7 | 32.0 | 1 | 4 | 2 |

| 5.282500 | 25.5 | 35.6 | 1 | 5 | 1 |

| 2.530000 | 25.6 | 36.4 | 1 | 6 | 2 |

| 0.364343 | 25.6 | 36.2 | 1 | 7 | 2 |

| 2.723870 | 31.9 | 39.4 | 1 | 8 | 2 |

| 3.520000 | 23.6 | 31.9 | 1 | 9 | 1 |

| 0.497500 | 19.5 | 25.0 | 1 | 10 | 2 |

| Note: One price per painting. Only first 10 observations. |

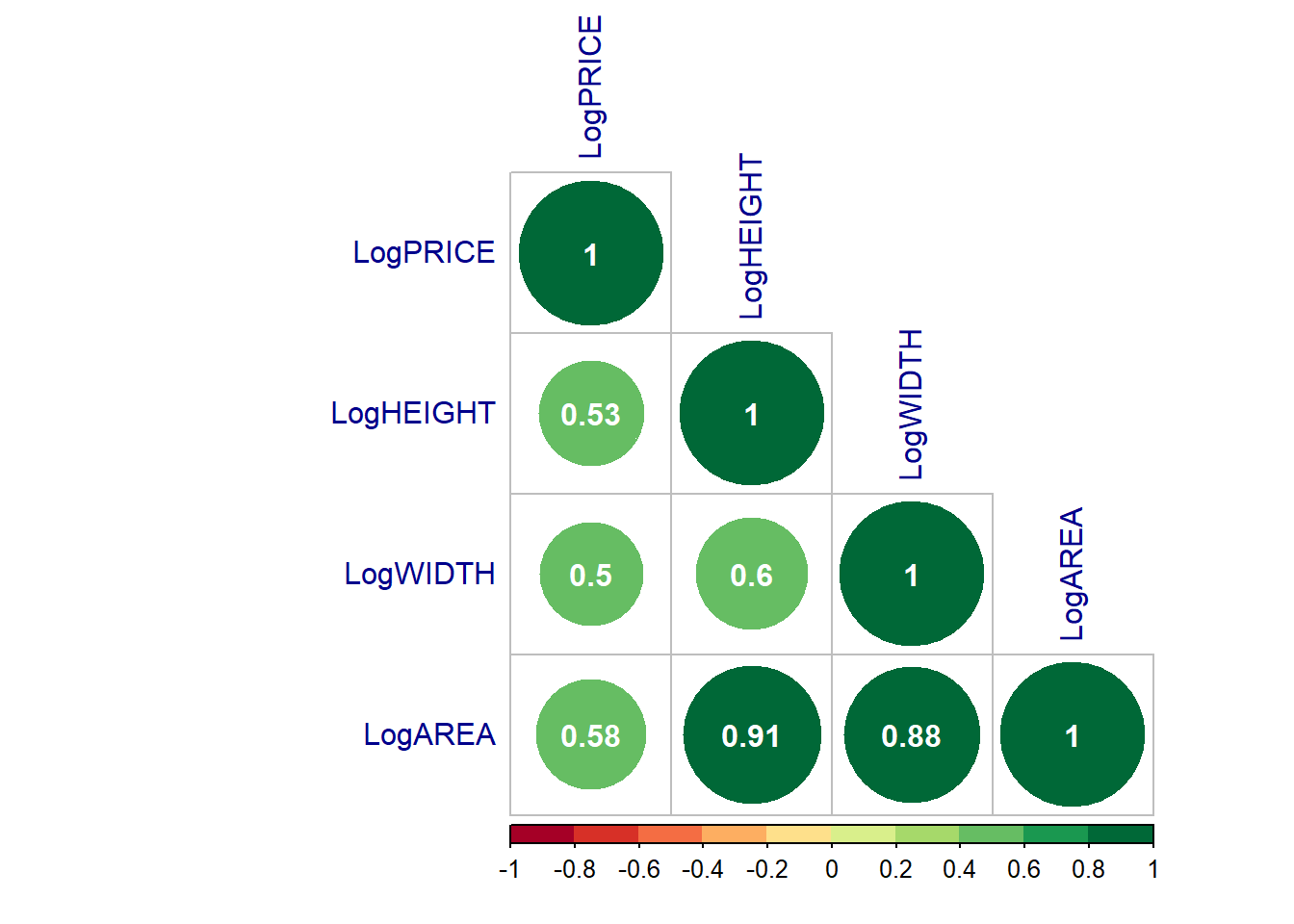

Figure 17.1: Graphical visualization of the correlation matrix

| LogPRICE | LogHEIGHT | LogWIDTH | LogAREA | |

|---|---|---|---|---|

| LogPRICE | 1.000 | 0.528 | 0.504 | 0.578 |

| LogHEIGHT | 0.528 | 1.000 | 0.599 | 0.907 |

| LogWIDTH | 0.504 | 0.599 | 1.000 | 0.880 |

| LogAREA | 0.578 | 0.907 | 0.880 | 1.000 |

Figure 17.2: Graphical visualization of the correlation matrix

The matrix above returns all pairwise correlations. Notice this is a symmetric matrix. Recall that correlation measures strength and direction of the linear relationship between to variables. The correlation between LogHEIGHT and LogAREA is extremely high, as well as the correlation between LogWIDTH and LogAREA.

Unlike exact collinearity, here we can still fit a model with all of the predictors, but what effect does this have?

- Model 0: \(\text{LogPRICE}_i = \beta_0 + \beta_1\text{LogHEIGHT}_i + \beta_2\text{LogWIDTH}_i+ \beta_3\text{LogAREA}_i+\epsilon_{i0}\)

.

. Call:

. lm(formula = LogPRICE ~ ., data = dataset)

.

. Residuals:

. Min 1Q Median 3Q Max

. -4.4778 -0.7111 -0.0832 0.7627 2.9904

.

. Coefficients: (1 not defined because of singularities)

. Estimate Std. Error t value Pr(>|t|)

. (Intercept) -8.4336 0.6569 -12.839 < 2e-16 ***

. LogHEIGHT 1.3545 0.2028 6.678 8.79e-11 ***

. LogWIDTH 1.2709 0.2284 5.565 5.01e-08 ***

. LogAREA NA NA NA NA

. ---

. Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

.

. Residual standard error: 1.11 on 373 degrees of freedom

. Multiple R-squared: 0.334, Adjusted R-squared: 0.3305

. F-statistic: 93.54 on 2 and 373 DF, p-value: < 2.2e-16Although the \(F-\)test for the regression tells us that the regression is significant, the parameter of LogAREA can not be defined because of singularities. Therefore, we fit alternative models:

Model 1: \(\text{LogPRICE}_i = \beta_0 + \beta_1\text{LogHEIGHT}_i+ \beta_2\text{LogWIDTH}_i+\epsilon_{i1}\)

Model 2: \(\text{LogPRICE}_i = \beta_0 + \beta_1\text{LogHEIGHT}_i+ \beta_3\text{LogAREA}_i+\epsilon_{i2}\)

Model 3: \(\text{LogPRICE}_i = \beta_0 + \beta_2\text{LogWIDTH}_i+ \beta_3\text{LogAREA}_i+\epsilon_{i3}\)

| Log PRICE | Log PRICE | Log PRICE | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable | Estimates | std. Error | p-value | Estimates | std. Error | p-value | Estimates | std. Error | p-value |

| (Intercept) | -8.43 | 0.66 | <0.001 | -8.43 | 0.66 | <0.001 | -8.43 | 0.66 | <0.001 |

| LogHEIGHT | 1.35 | 0.20 | <0.001 | 0.08 | 0.39 | 0.829 | |||

| LogWIDTH | 1.27 | 0.23 | <0.001 | -0.08 | 0.39 | 0.829 | |||

| LogAREA | 1.27 | 0.23 | <0.001 | 1.35 | 0.20 | <0.001 | |||

| Observations | 376 | 376 | 376 | ||||||

| R2 / R2 adjusted | 0.334 / 0.330 | 0.334 / 0.330 | 0.334 / 0.330 | ||||||

One of the first things we should notice is that parameters of LogHEIGHT and LogWIDTH have a large change in the value and they are not significant when LogAREA is included as regressor in the same model (Model 2 and Model 3).

Another interesting result is the opposite signs of the coefficient for LogWIDTH in Model 1 and Model 2. This should seem rather counter-intuitive. Increasing WIDTH increases or decreases PRICE?

Moreover, the value of the parameter of LogAREA in Model 2 is similar to the value of the parameter of LogWIDTH in Model 1. The value of the parameter of LogAREA in Model 2 is similar to the value of the parameter of LogHEIGHT in Model 1.

This happens as a result of the predictors being highly correlated.

When LogAREA and LogHEIGHT are both in the model, their effects on the response are lessened individually, but together they still explain a large portion of the variation of LogPRICE .

Another way to inspect for Multicollineary is using regressions between regressors, like:

- Model A1: \(\text{LogAREA}_i = \alpha_0 + \alpha_1 \text{LogHEIGHT}_i + e_{i1}\)

- Model A2: \(\text{LogAREA}_i = \alpha_0 + \alpha_2 \text{LogWIDTH}_i + e_{i2}\)

| Log AREA | Log AREA | |||||

|---|---|---|---|---|---|---|

| Variable | Estimates | std. Error | p-value | Estimates | std. Error | p-value |

| (Intercept) | 1.69 | 0.12 | <0.001 | 0.95 | 0.16 | <0.001 |

| LogHEIGHT | 1.53 | 0.04 | <0.001 | |||

| LogWIDTH | 1.67 | 0.05 | <0.001 | |||

| Observations | 376 | 376 | ||||

| R2 / R2 adjusted | 0.823 / 0.822 | 0.775 / 0.774 | ||||

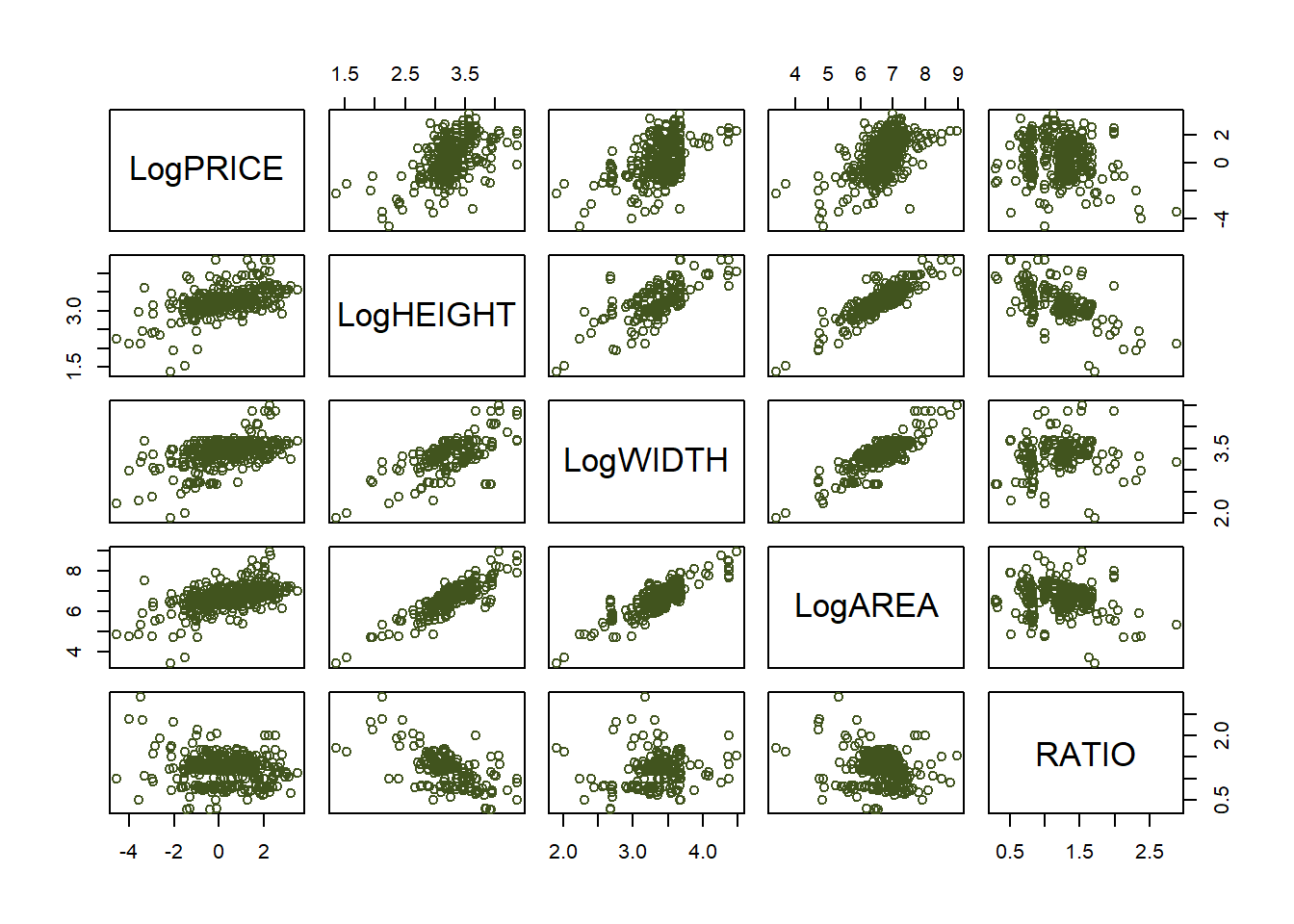

17.7.7 Revisiting Monet Case

For illustrative purposes, we add a small random noise to the variable AREA - that is, AREA is not an exact combination of HEIGHT and WIDTH - and we create a new variable: RATIO.

\[\begin{align} \text{LogAREA}=\log ( WIDTH \times HEIGHT) + \varepsilon; \,\,\, \varepsilon \sim N(0,0.2) \end{align}\]

\[\begin{align} \text{RATIO}= \dfrac{WIDTH}{HEIGHT} \end{align}\]

| LogPRICE | LogHEIGHT | LogWIDTH | LogAREA | RATIO | |

|---|---|---|---|---|---|

| LogPRICE | 1.000 | 0.528 | 0.504 | 0.551 | -0.162 |

| LogHEIGHT | 0.528 | 1.000 | 0.599 | 0.855 | -0.577 |

| LogWIDTH | 0.504 | 0.599 | 1.000 | 0.839 | 0.272 |

| LogAREA | 0.551 | 0.855 | 0.839 | 1.000 | -0.187 |

| RATIO | -0.162 | -0.577 | 0.272 | -0.187 | 1.000 |

Model 1: \(\text{LogPRICE}_i = \beta_0 + \beta_1\text{LogHEIGHT}_i \epsilon_{i1}\)

Model 2: \(\text{LogPRICE}_i = \beta_0 + \beta_2\text{LogWIDTH}_i + \epsilon_{i2}\)

Model 3: \(\text{LogPRICE}_i = \beta_0 + \beta_3\text{LogAREA}_i + \epsilon_{i3}\)

Model 4: \(\text{LogPRICE}_i = \beta_0 + \beta_1\text{LogHEIGHT}_i + \beta_2\text{LogWIDTH}_i+ \beta_3\text{LogAREA}_i + \epsilon_{i4}\)

Model 5: \(\text{LogPRICE}_i = \beta_0 + \beta_1\text{LogHEIGHT}_i + \beta_3\text{LogAREA}_i + \epsilon_{i5}\)

Model 6: \(\text{LogPRICE}_i = \beta_0 + \beta_2\text{LogWIDTH}_i+ \beta_3\text{LogAREA}_i + \epsilon_{i6}\)

| Log PRICE | Log PRICE | Log PRICE | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable | Estimates | std. Error | p-value | Estimates | std. Error | p-value | Estimates | std. Error | p-value |

| (Intercept) | -6.29 | 0.55 | <0.001 | -7.15 | 0.66 | <0.001 | -7.72 | 0.63 | <0.001 |

| LogHEIGHT | 2.03 | 0.17 | <0.001 | ||||||

| LogWIDTH | 2.18 | 0.19 | <0.001 | ||||||

| LogAREA | 1.21 | 0.09 | <0.001 | ||||||

| Observations | 376 | 376 | 376 | ||||||

| R2 / R2 adjusted | 0.279 / 0.277 | 0.254 / 0.252 | 0.304 / 0.302 | ||||||

| Log PRICE | Log PRICE | Log PRICE | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable | Estimates | std. Error | p-value | Estimates | std. Error | p-value | Estimates | std. Error | p-value |

| (Intercept) | -8.44 | 0.66 | <0.001 | -7.73 | 0.63 | <0.001 | -8.09 | 0.66 | <0.001 |

| LogHEIGHT | 1.28 | 0.35 | <0.001 | 0.81 | 0.32 | 0.011 | |||

| LogWIDTH | 1.20 | 0.37 | 0.001 | 0.62 | 0.34 | 0.073 | |||

| LogAREA | 0.07 | 0.29 | 0.804 | 0.81 | 0.18 | <0.001 | 0.94 | 0.17 | <0.001 |

| Observations | 376 | 376 | 376 | ||||||

| R2 / R2 adjusted | 0.334 / 0.329 | 0.316 / 0.312 | 0.310 / 0.306 | ||||||

Including RATIO:

Model 7: \(\text{LogPRICE}_i = \beta_0 + \beta_4\text{RATIO}_i \epsilon_{i7}\)

Model 8: \(\text{LogPRICE}_i = \beta_0 + \beta_3\text{LogAREA}_i + \beta_4\text{RATIO}_i + \epsilon_{i8}\)

Model 9: \(\text{LogPRICE}_i = \beta_0 + \beta_1\text{LogHEIGHT}_i + \beta_4\text{RATIO}_i + \epsilon_{i9}\)

| Log PRICE | Log PRICE | Log PRICE | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable | Estimates | std. Error | p-value | Estimates | std. Error | p-value | Estimates | std. Error | p-value |

| (Intercept) | 1.14 | 0.27 | <0.001 | -7.24 | 0.72 | <0.001 | -8.92 | 0.85 | <0.001 |

| RATIO | -0.67 | 0.21 | 0.002 | -0.25 | 0.18 | 0.165 | 0.89 | 0.22 | <0.001 |

| LogAREA | 1.18 | 0.10 | <0.001 | ||||||

| LogHEIGHT | 2.51 | 0.20 | <0.001 | ||||||

| Observations | 376 | 376 | 376 | ||||||

| R2 / R2 adjusted | 0.026 / 0.024 | 0.307 / 0.303 | 0.309 / 0.306 | ||||||

References:

- Adapted from Statistics for Business and Economics Chapter 13. Additional Topics in Regression Analysis. Copyright (c) 2013 Pearson Education.

- Examples taken from Applied Statistics with R

a concept we will return to later↩︎